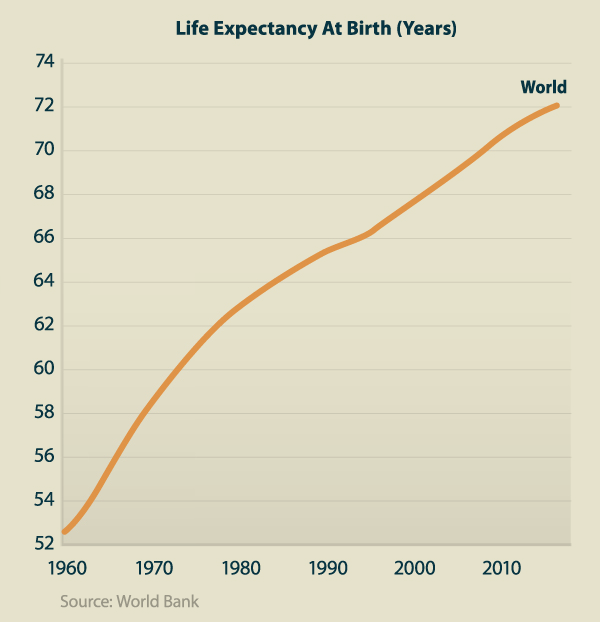

Most of us are aware of the financial risks associated with the Investment portfolios, businesses, or retirement plans. Some of these risks are controllable while others are not – the Market risk is an example of the prior while Financial risk/Credit risk falls in the latter category. Managing these risks is an important part of managing your business, investments or savings plan. One such risk which has emerged in a big way is the Longevity risk – which describes what would happen if you were to Outlive your savings. This is a real worry in today’s World as lifespans continue to get longer with drastic improvements in Healthcare technology, Lifestyle changes & socio-economic status. The graph below shows how Global Life expectancy has jumped almost 40% from around 52 years in 1960 to over 72 years in 2010. As evident People are living longer today – they need bigger investment portfolios to sustain themselves after retirement.

Despite the data, people still underestimate their life expectancy for two reasons – comparing themselves to older relatives & quoting life expectancy at the birth statistic, both of which are misleading… here’s Why? According to U.S Library of National Medicine, only 25% of the variation in lifespan is based on ancestry, but it’s certainly not the only factor. Gender, lifestyle, Diet are some of the other factors that contribute towards your lifespan. For the second metric, people fail to realize is that while their expected lifespan might be shorter at the time of their birth but it continues to increase during their lifetime. According to an OECD study for expected Age of death as of 2016 in the U.S climbed from 72 to 86 for Men & 82 to 89 for Women during their lifetime. Couple the longer lifespans & inaccurate life expectancy predictions with the lack of retirement savings in the U.S households (figure below) & we have a bigger problem at our hands. According to the data, 35% of the U.S households don’t even have any retirement savings whatsoever. This is where Longevity Risk enters into the picture.

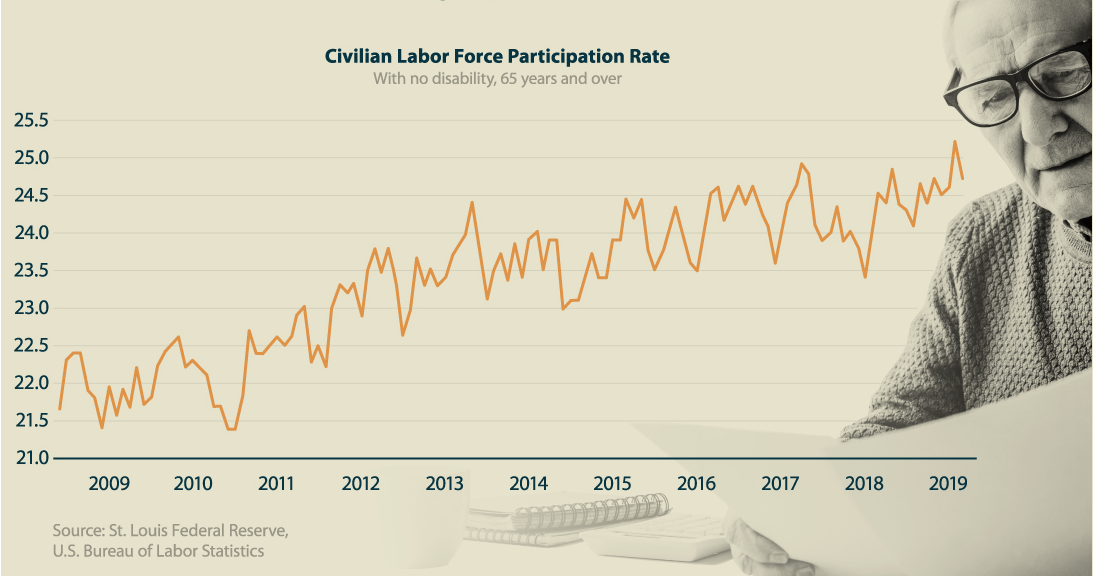

Combining all these factors many people are facing a real problem of outliving their savings. To combat this situation, the simplest & most common solution that is emerging is of Older individuals (over 65) are working longer to make up for the difference. This is evident from The Labor force participation rate for Seniors that has been steadily trending upwards for in the past decade in the U.S (figure below). But this alone can’t combat the Longevity Risk. And to top all of this, the problem is not restricted to Seniors alone – according to Federal Reserve, 41% of the U.S Millennials (aged 18-29) have no retirement savings & prefer to keep cash.

How do you solve this problem? One solution lies in the right mix of asset allocation in the investors’ portfolio. The “100-age” rule provides a guideline on the kind of asset allocation mix one should have as the age progresses. Basically your age should match the proportion of stocks (high risk-high return) and bonds (low risk-low return) that one should have in their investment portfolio to manage risk exposure effectively. So for example, a person aged 25 who has just started working & looking at a long career in front of him would opt for 25% of bonds & 75% of stocks, since they are not risk averse at this stage of life & also looking for growth. On the other hand, a 65-year-old who is looking to retire soon would look at 65% of asset allocation to be in safe but low-risk investments since their aim at this age is the preservation of their retirement capital. With the rise in life expectancies & lengthening time horizons, Financial advisers are even suggesting a 110 or 120-age rule to their clients.

How do you solve this problem? One solution lies in the right mix of asset allocation in the investors’ portfolio. The “100-age” rule provides a guideline on the kind of asset allocation mix one should have as the age progresses. Basically your age should match the proportion of stocks (high risk-high return) and bonds (low risk-low return) that one should have in their investment portfolio to manage risk exposure effectively. So for example, a person aged 25 who has just started working & looking at a long career in front of him would opt for 25% of bonds & 75% of stocks, since they are not risk averse at this stage of life & also looking for growth. On the other hand, a 65-year-old who is looking to retire soon would look at 65% of asset allocation to be in safe but low-risk investments since their aim at this age is the preservation of their retirement capital. With the rise in life expectancies & lengthening time horizons, Financial advisers are even suggesting a 110 or 120-age rule to their clients.

Simple rules of thumb as discussed above provide an easy understanding of the investment criterion, they shouldn’t be treated as the only policy tool. Every person has a unique situation, risk profile, investment objectives, lifestyle & net worth which eventually dictate the overall make of their portfolio. Here are some of the things which can help reduce the Longevity risk.

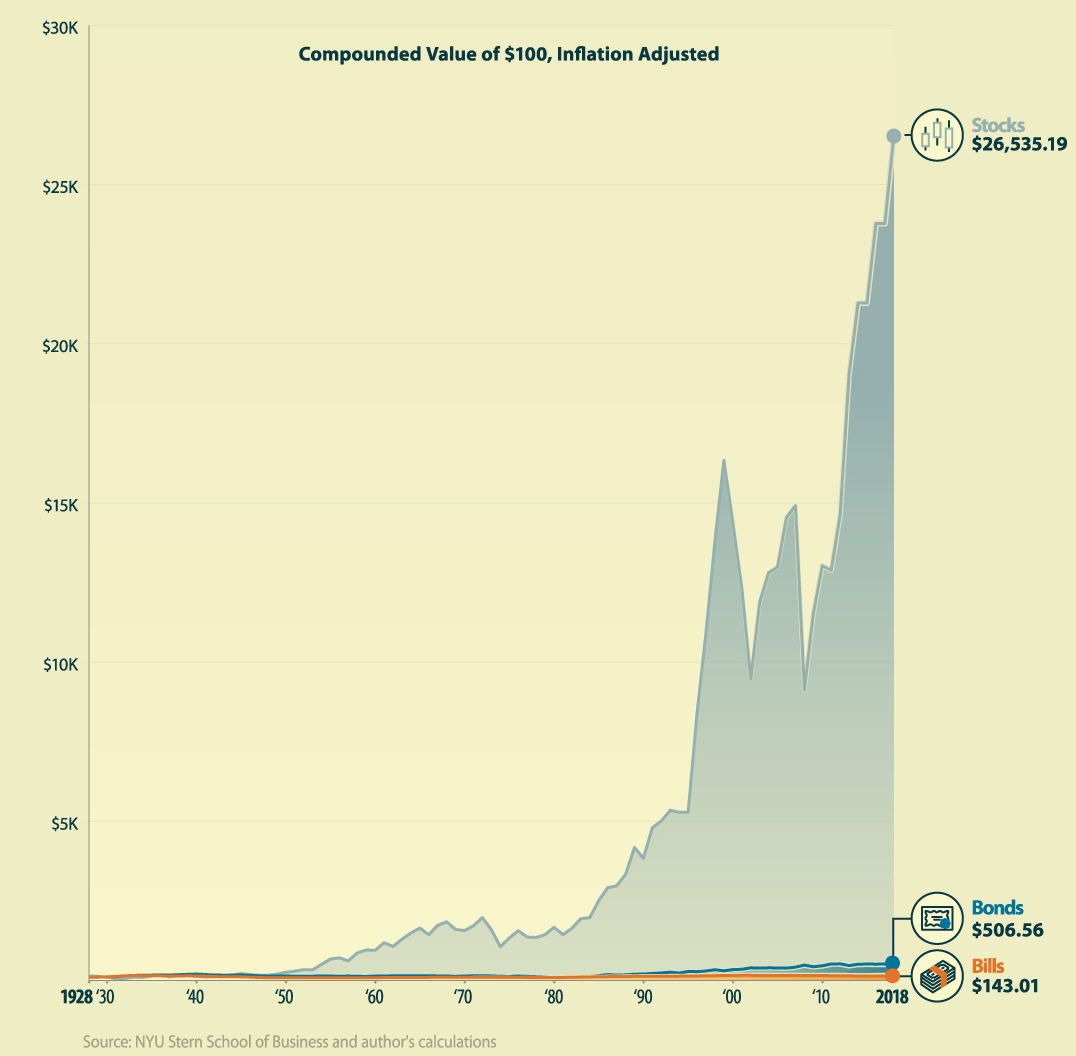

- Historically speaking, Equities have provided a much higher rate of return than other asset classes. The comparable returns between U.S treasury bills, Bonds & Stocks have a huge difference as you can see in the chart above. Not only this but stocks provide added value with investment returns in the form of dividends for the reinvested capital.

- Small Yearly withdrawals can reduce the risk of downside in Equities. Let’s assume a retired 65-year-old has a retirement account $1M & last year market takes a hit of 20% reducing his savings to $800K. If he withdraws 4% of his original portfolio ($40K), his net loss would only by $8,000 (4% of $800K). Overtime his withdrawal with the fluctuating market would average out his returns.

- Working beyond the Retirement age can increase the potential of Earnings and also reduce the effect of Market downside on the retirement portfolio. In this case, Seniors are better equipped to recoup any losses they incur in the short-term while maximizing the returns from continued investment in Equities.

- According to PWC, Baby boomers are forecasted to transfer $30 trillion to younger generations over the next 30 years. Many well-off individuals want to leave the next of kin in a financially secure position. For this, their retirement portfolio withdrawals will only occur after their passing away. The longer investment time horizon ensures that the portfolio weathers the short-term market risks by maximizing returns in the long run.

Holding Equities is an effective way to battle the longevity risk since stocks deliver desired results in the long-term. Having said that this requires a lot of psychological discipline – investors need to control their emotions in ups & downs of the market while eyeing the long-term perspective.

Email ?| Twitter ? | LinkedIn ?| StockTwits ? | Telegram ?